By Roberto Ferrigno, European Bioeconomy Bureau

The European Commission has officially adopted its new Bioeconomy Strategy—marking an important step toward a more competitive, climate-neutral, and resilient Europe.

The updated strategy puts the spotlight on three priorities: scaling sustainable bio-based industries, deploying local and regional bioeconomies, and ensuring that Europe’s use of biological resources stays within ecological limits.

Several concrete actions stand out. The Commission will support the scale-up of biorefineries and bio-based materials, strengthen investment through dedicated platforms and EU partnerships, and accelerate innovation in biotechnology and biomanufacturing. A new Strategic Deployment Agenda will help regions build their own bioeconomy pathways, supported by living labs, pilot actions, and tailored policy assistance.

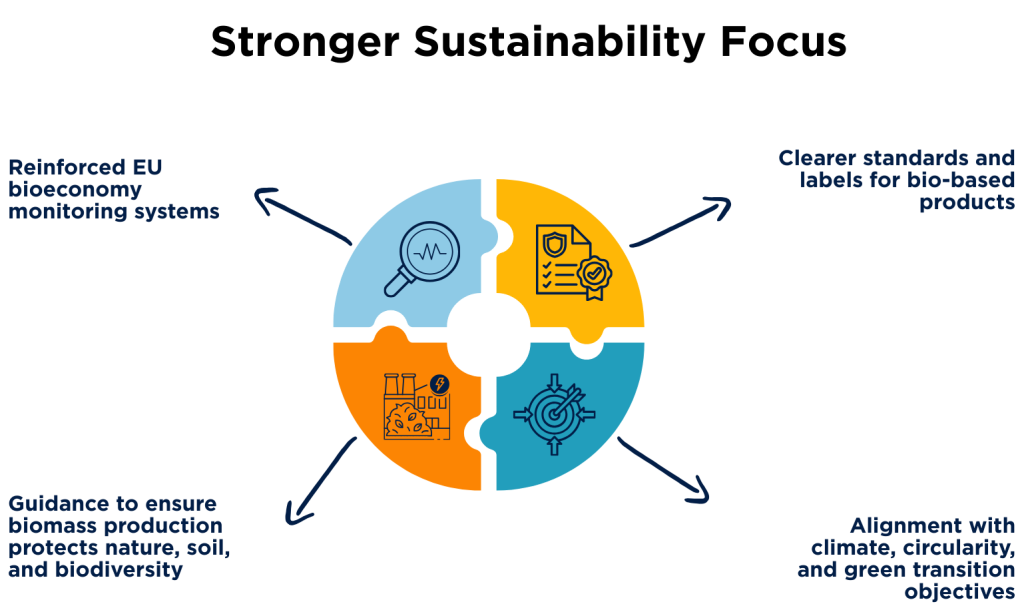

Equally important is the renewed focus on sustainability. The strategy reinforces EU monitoring systems, promotes clearer standards and labels for bio-based products, and provides guidance to ensure that biomass production protects nature, soils, and biodiversity.

In short, the strategy sets a clearer direction: a bioeconomy that boosts European competitiveness, creates rural opportunities, and contributes to climate and circularity goals—while staying grounded in environmental responsibility.

A strong signal that Europe sees the bioeconomy not just as a sector, but as a strategic pillar for its green and industrial transitions.

The widespread calls from many stakeholders including EBB and its partners for strong mechanisms that create markets for biotechnology products are unanswered. The absence of market pulls such as targets, mandates and obligations hinders the transition from fossil based to plant based feedstocks and their transformation into innovative materials. We hope this absence of market mechanisms is addressed in the specific enabling acts.

Bioeconomy Implementation – EU Legislative Levers Dashboard (2025–2030)

Below is a concise dashboard of the main EU legislative levers that will be used (or are being proposed) to implement the key objectives of the EU Bioeconomy Strategy. It covers what each lever is, status & timeline (2025–2030), why it matters for the bioeconomy/biorefineries, implementation risks, and quick mitigation steps.

| What it is/role | Status & timeline (key dates) | Why it matters for bioeconomy / biorefineries | Implementation risks (2025–2030) | Mitigation / policy actions | |

| Industrial Accelerator Act (IAA) | Clean-industry package to speed permitting, create low-carbon product criteria and preference in procurement, and support industrial clusters. Creates “lead markets” for low-carbon / bio-based products. | Proposal announced under the Clean Industrial Deal; Commission scheduled for Q4 2025 (adoption planning Dec 2025 in trackers). | Can create demand-side pull (procurement + EU content / sustainability criteria), speed permitting for biorefineries, and reduce project timelines. Strong lever to de-risk investments. | Name/scope shifting; political negotiation may dilute procurement / EU-content rules; permitting measures may be slow in practice. | Keep EU content & sustainability criteria robust; set clear delegated-act timelines; require Member State permit fast-track pilots for biorefineries. |

| Ecodesign for Sustainable Products Regulation (ESPR) + Digital Product Passport (DPP) | Framework to set product requirements (durability, recyclability, material content) and DPPs for traceability of materials, including bio-carbon content. | ESPR entered into force 18 July 2024; Commission rolled out first product sets and horizontal rules in 2025 and is developing working plans for more products. DPP rollouts are ongoing. | ESPR/DPPs enable traceability of bio-based content, allow ecodesign criteria to favour bio-based materials, and make product claims verifiable — key for market acceptance. | Complexity of DPP data requirements; compliance costs for SMEs; risk of inconsistent metrics for “bio-carbon” and LCA. | Create tiered DPP requirements for SMEs; EU guidance on bio-carbon accounting; align DPPs with sustainability certification schemes. |

| Circular Economy Act (CEA) / Clean Industrial Deal measures | System-level regulatory framework to raise circularity (targets, lead markets, streamlined rules). Supports product and material system reforms. | Public consultation launched in 2025; the CEA remains a priority action in the Clean Industrial Deal with timelines through 2026–2028 for legislative proposals and implementation. | Can set economy-wide targets (e.g., higher circularity by 2030), prioritize bio-based materials in supply chains and public procurement, and support enabling infrastructure for biorefineries. | Potential policy fragmentation; trade-offs between recycling targets and bio-based material uptake; industry pushback. | Ensure policy coherence (align CEA with ESPR & IDAA); set sectoral pathways that balance recycling and renewable-carbon needs. |

| CBE JU – Circular Bio-based Europe (funding & flagship projects) | Joint Undertaking funding demonstration & flagship biorefineries, R&I and scale-up. Provides grant / de-risking finance for first-of-a-kind plants. | Active with calls: 2025 Horizon-JU CBE call launched April 2025 (budget €172m); ongoing project map of demo plants/flagships. | Directly finances demo biorefineries, lowers technical & commercial risk, accelerates scale-up of bio-based materials and supply chains. | Funding scale still limited relative to investment needs; time-to-market for funded flagships can be long. | Scale budgets (blended finance), link CBE JU projects with IPCEI/state aid for large-scale deployment, prioritise replication pathways for rural biorefineries. |

| IPCEIs (Important Projects of Common European Interest) | State-aided cross-border strategic projects — can mobilize large public & private capital for strategic value chains (e.g., biomanufacturing). | IPCEI tool already used in EU (approved projects ongoing). Member States are exploring biotech/biobased IPCEIs. Approvals continue on demand. | Allows national / cross-border state aid to unlock very large investments (industrial biorefineries, Value Chain hubs) that otherwise wouldn’t attract private capital. | Political complexity (state aid scrutiny), uneven Member State participation → geographic concentration of projects. | Encourage multi-Member State consortia; set clear sustainability & local benefit conditions; link to CAP / cohesion funding for regional inclusion. |

| European Chemicals Industry Action Plan & regulatory alignment | Action plan to strengthen chemicals sector, accelerate decarbonisation and foster lead markets for strategic chemicals (including bio-based). | Action plan published (2025); measures include industry partnerships, possible fiscal incentives, and “critical chemicals” initiatives. | Can prioritize bio-based chemicals as strategic; create incentives (tax, procurement) and supply-security measures to favor bio-derived feedstocks. | Risk: trade remedies / competitiveness tensions; possible protectionist pressures; fragmentation with chemical REACH rules. | Use harmonized sustainability criteria; combine support with open market rules and export strategies; integrate bio-based goals into REACH-related guidance where relevant. |

| Public Procurement & Green Procurement Rules | EU-level procurement rules embedding sustainability / EU preference (via IDAA & sector legislation). | Being designed as part of IDAA and Clean Industrial Deal — with procurement criteria for low-carbon / EU-content products rolling out post-2025. | Creates guaranteed initial demand for bio-based materials (construction, packaging, public services), accelerating market uptake. | Risk of procurement rules being watered down; administrative overload for procurers. | Publish sectoral procurement templates (bio-based criteria); run pilot procurements for bio-based goods and build buyer guidance. |

| Sustainability certification & standards (labels) | Standards for “bio-based”, “renewable carbon”, and LCA-based labels feeding into ESPR, procurement & product claims. | Driven by Commission strategy & standardisation bodies; several initiatives ongoing through 2025–2027 to define metrics. | Reliable labels are essential to avoid greenwashing, enable DPP transparency, and create price premium for certified bio-based materials. | Fragmented standards; inconsistent metrics for “biogenic carbon” and LCA results. | Fast-track EU common methodology for renewable carbon; require third-party verification and align with DPP data fields. |

Five Load-Bearing Facts (sources)

- The ESPR is in force (18 July 2024) and already begins to require DPPs and sustainability criteria — a structural tool for product-level intervention.

- The Clean Industrial Deal (Feb 2025) and the planned Industrial Decarbonisation Accelerator Act are explicit EU efforts to create lead markets and speed permitting for clean industrial projects; IDAA was slated for Q4 2025.

- The Circular Bio-based Europe Joint Undertaking (CBE JU) is actively funding demonstration and flagship biorefinery projects (calls in 2025; map of projects).

- The Commission’s Chemicals Industry Action Plan (2025) positions bio-based chemicals as strategic and proposes measures (incentives, market support) that intersect with bioeconomy goals.

- The IPCEI framework is a proven route to mobilise large state & private investment for strategic industrial value chains; Member States have used it for batteries, hydrogen and are exploring biotech use.

Quick Risk Scorecard (2025–2030) – Likelihood × Impact

- Regulatory fragmentation (high likelihood × high impact) — score: High. (Multiple overlapping acts need alignment.)

- Data & verification bottlenecks (DPP & LCA) (medium × high) — score: High.

- Funding gap vs. investor appetite (medium × high) — score: High.

- Member State uneven implementation (high × medium) — score: High–Medium.

- Technology readiness / scale delays (medium × medium) — score: Medium.

Priority Actions EU should take (to maximise impacts, short checklist)

- Harmonise metrics: mandate a single EU methodology for renewable carbon / bio-carbon accounting and DPP data fields (urgent).

- Link finance to regulation: allocate larger blended-finance packages that top-up CBE JU grants and steer IPCEI calls to bio-based scale-ups.

- Procurement pilots: run targeted public procurement for bio-based construction, packaging & municipal goods to create demand signals.

- Permitting pilots: require Member States to set up fast-track permitting for biorefineries under IDAA pilot rules.

- SME support & DPP tiers: reduce burden for SMEs by tiering DPP requirements and offering technical assistance.

The project is supported by the Circular Bio-based Europe Joint Undertaking and its members under grant agreement Nº 101157907. Funded by the European Union. Views and opinions expressed are however those of the author(s) only and do not necessarily reflect those of the European Union or CBE JU. Neither the European Union nor the CBE JU can be held responsible for them.